The Price-to-Earnings (P/E) ratio is a fundamental financial metric used to assess the relative valuation of a company’s stock. It is one of the investment community’s most widely used and discussed ratios. The P/E ratio is calculated by dividing a company’s stock’s current market price per share by its earnings per share (EPS) over a specific period (usually the last 12 months or the projected earnings for the next 12 months).

What is P/E Ratio?

P/E ratio is a financial metric used to evaluate the relative valuation of a company’s stock. It is calculated by dividing the current stock price by the earnings per share (EPS) of the company.

The formula for the P/E ratio is:

P/E Ratio = Stock Price / Earnings per Share (EPS)

EPS stands for Earnings Per Share. It is a financial metric that measures a company’s profitability on a per-share basis. EPS is calculated by dividing a company’s net earnings (profit after taxes and preferred dividends) by the weighted average number of outstanding shares during a specific period (usually the last 12 months or the quarterly period).

The formula for calculating EPS is as follows:

EPS = (Net Earnings - Preferred Dividends) / Weighted Average Number of Outstanding Shares

EPS is an essential indicator for investors as it provides insights into how much profit the company is generating for each outstanding share. Higher EPS generally indicates higher profitability and better financial performance.

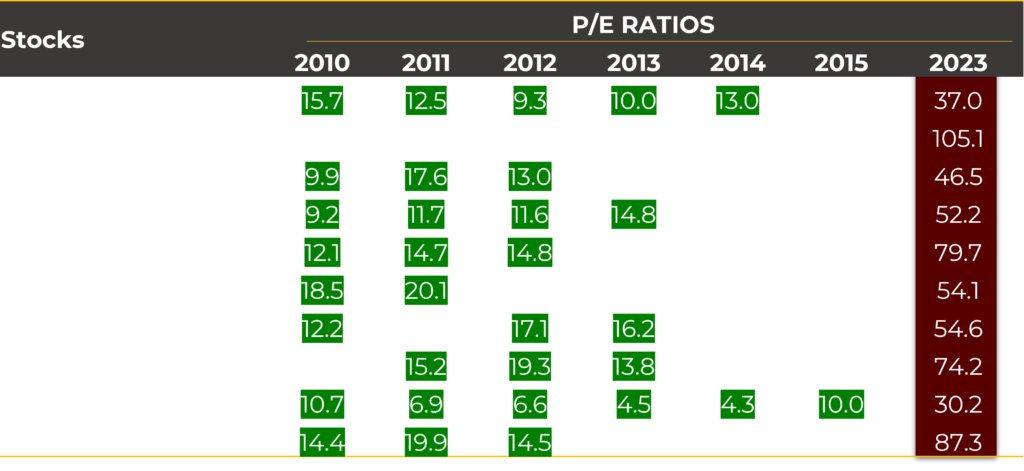

A low Price-Earnings (P/E) ratio can be a critical indicator in identifying a potential multibagger investment opportunity. A low PE ratio implies that a company’s stock is trading at a relatively low multiple of its earnings, making it more attractively priced compared to its earnings potential. This could signal that the market has undervalued the stock, providing an opportunity for significant future growth. Companies with low PE ratios may be operating in sectors with temporary challenges or overlooked growth prospects, and as these challenges are overcome, their earnings could substantially increase, driving the stock price higher. Here are some of our observations of the historical P/E of today’s multibagger stocks.

Why PE Ratio Alone Isn't Enough for Smart Investing?

Looking beyond the P/E ratio is essential because it has limitations in providing a comprehensive view of a company’s financial health and performance. Considering other financial ratios, such as ROCE, ROE, and capital efficiency, helps assess profitability, operational efficiency, and growth potential, offering a more holistic analysis for making informed investment decisions. Relying solely on P/E ratio may lead to overlooking crucial factors like debt levels, cyclical nature of businesses, and overall industry trends, which can significantly impact the company’s long-term prospects.

A stock with a P/E multiple of 100x may appear more expensive than one with a 20x P/E multiple, even if both stocks experience the same profit growth. However, this seeming disparity can be attributed to factors like superior capital efficiency, as measured by Return on Capital Employed (ROCE), and the long-term compounding of free cash flow. Additionally, companies that focus on enhancing capital efficiencies over time may justify a higher P/E multiple compared to their own historical P/E. In valuing Consistent Compounders, Discounted Cashflows more accurately account for these distinctive characteristics rather than relying solely on P/E multiples.

Debunking Two Common Misconceptions in P/E Multiples-Based Valuation

Misconception #1: Comparing P/E Multiples for Equal Profit Growth Rates.

In this analysis, we examine two stocks, A and B, with different P/E multiples (20x and 100x, respectively) but the same expected earnings growth rate of 10% CAGR. While it might seem that Stock B is overvalued compared to Stock A, we reveal how considering the ‘capital efficiency’ of the underlying businesses can lead to a more accurate valuation.

The intrinsic value of a stock depends on its expected free cash flows, which are influenced not only by earnings growth but also by how efficiently the company utilizes its capital. By calculating the Return on Capital Employed (RoCE) for both stocks, we find that Stock B is significantly more capital efficient than Stock A, generating four times more free cash flows with the same growth rate.

Suppose the Return on Capital Employed (RoCE) for Stock A is 12% and for Stock B is 30%. Both stocks have current profits valued at Rs 150, however, stock B will be more valuable given a higher ROCE. Let us understand with step by step analysis:

Given data:

– Return on Capital Employed (RoCE) for Stock A = 12%

– Return on Capital Employed (RoCE) for Stock B = 30%

– Current profits for both stocks = Rs 150

Step 1: Calculate the capital employed for each stock.

– Capital employed for Stock A = Rs 150 / 12% = Rs 1250

– Capital employed for Stock B = Rs 150 / 30% = Rs 500

Step 2: Calculate the incremental capital required to achieve an 10% earnings growth next year.

– Earnings growth = Rs 150 * 10% = Rs 15

For Stock A:

– Incremental capital required = Rs 15 / 12% = Rs 125

– Free cash flows (FCF) = Current profits – Incremental capital = Rs 150 – Rs 125 = Rs 25

For Stock B:

– Incremental capital required = Rs 15 / 30% = Rs 50

– Free cash flows (FCF) = Current profits – Incremental capital = Rs 150 – Rs 50 = Rs 100

Step 3: Calculate the FCF multiple for each stock.

– FCF multiple for Stock A = FCF / Current profits = Rs 25 / Rs 150 = 0.17x

– FCF multiple for Stock B = FCF / Current profits = Rs 100 / Rs 150 = 0.67x

Step 4: Calculate the fair value P/E multiple for each stock.

– Fair value P/E multiple for Stock A = 1 / FCF multiple = 1 / 0.17 ≈ 5.88x

– Fair value P/E multiple for Stock B = 1 / FCF multiple = 1 / 0.67 ≈ 1.49x

Given the capital efficiency, Stock B is approximately 1.5 times (6.67/ 4) more capital efficient than Stock A. Therefore, the fair value P/E multiple for Stock B should be around 1.5 times that of Stock A. If the fair value P/E of Stock A is 5.9x, the fair value P/E of Stock B should be approximately 1.5 * 5.9 ≈ 8.85x. This implies that at its currently prevalent P/E of 100x, Stock B is undervalued compared to Stock A, which trades at 20x P/E. In other words, Stock B, trading at 100x P/E, is actually considered ‘cheap’ compared to Stock A trading at 20x P/E.

Misconception #2: P/E multiples tend to revert to the mean for companies continually enhancing their capital efficiency.

The concept of capital efficiency extends not only across different companies but also within a single company over time. If a company continuously improves its capital efficiency through higher asset turnover, reduced incremental capex, technological advancements in the supply chain, and increased bargaining power, its historical P/E or P/B ratios become incomparable to the current prevalent price multiples.

The underlying assumption behind these concerns is that, as P/E multiples surpass past averages, ‘mean reversion’ is likely to occur. Nevertheless, if the company continuously enhances its capital efficiency, as measured by Return on Capital Employed (RoCE), it will experience much faster growth in free cash flows compared to earnings. As a result, P/E multiples become less relevant, and comparing the firm’s current P/E with its historical P/E becomes invalid.

Discover the secrets of identifying high-quality stocks with ease, faster than preparing a cup of coffee, by joining our exclusive Hybrid Investing Masterclass!

Learn To Build Your Multi-bagger Portfolio Spending Only 15 Minutes Without Finance Knowledge Or Investing Experience Without Losing Your Mind And Money

Learn how to recognize businesses with strong moats, prudent capital allocation, and a relentless focus on achieving operational efficiencies. In this masterclass, you will uncover why valuations of such exceptional businesses should never rely solely on P/E multiples. They inherently deserve higher P/E multiples compared to lower quality businesses and even their own historical P/E multiples, cementing their position as top-tier investment opportunities.

Disclaimer:

This blog/video is for educational purposes only and should not be considered financial advice. It is essential to conduct your own research and consult with a qualified financial advisor before making any investment decisions. Your personal financial situation, risk tolerance, and investment goals are unique, and this content may not be suitable for you. Please make informed decisions based on your specific circumstances and professional guidance.